NY Times- Health – By REED ABELSON-OCT. 20, 2017

Despite President Trump’s pronouncements, not only is Obamacare not dead, there are signs that his administration is keeping it alive.

In the latest signal that the Affordable Care Act is still law, the Internal Revenue Service said this week that it is taking steps to enforce the most controversial provision: the tax penalty people face if they refuse to obtain health insurance.

Next year, for the first time, the I.R.S. will reject your tax return when filed electronically if you do not complete the information required about whether you have coverage, including whether you are exempt from the so-called individual mandate or will pay the penalty. If you file your tax return on paper, the agency said it could suspend processing of the return and delay any refund you might be owed.

The agency’s new guidance for tax professionals seems to contradict Mr. Trump’s first executive order, on Inauguration Day, which broadly instructed various agencies to scale back the regulatory reach of the federal health care law.

As part of his promise to overturn the law, the executive order hinted that the new administration could stop enforcing the mandate that people have insurance or pay a tax penalty, which proponents have long argued is critical to the law’s success by requiring young and healthy people to enroll.

The I.R.S.’s guidance makes it clear that taxpayers cannot simply ignore the Affordable Care Act. While the penalty applies only to people without insurance, all taxpayers are required to say whether they have coverage.

Legal experts say the I.R.S. has been clear that the law was in effect, despite repeated efforts by Mr. Trump and Republican lawmakers to repeal it. Congress would have to specifically repeal the mandate, they say, even if the administration has significant leeway over how aggressively it enforces it.

“This guidance should put to rest speculation that the I.R.S. is no longer enforcing the individual mandate and improve compliance,” wrote Timothy Jost, an emeritus law professor at Washington and Lee University in a recent analysis.

But there has been substantial confusion among taxpayers and insurers. Many insurance companies raised their rates for next year’s plans because they were worried the administration would essentially stop penalizing people who refused to buy coverage, leading to fewer enrollments, said Sabrina Corlette, a research professor at Georgetown University.

People may have also mistakenly believed they did not have to comply with the law’s reporting requirements. The new guidance suggests taxpayers will now face a sharp reminder that they need to provide this information, when they go to file a return electronically or submit the appropriate paperwork to get any refund they are due.

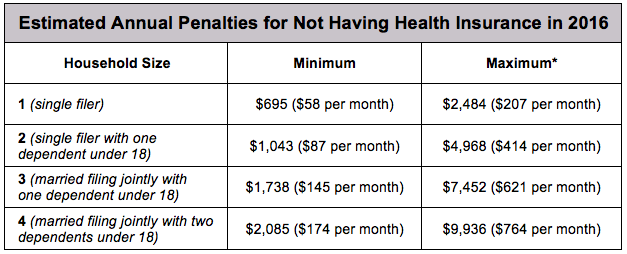

Under the law, an individual who does not have insurance can face a penalty of $695 a year for an individual, up to a maximum of $2,085 for a family or 2.5 percent of your adjusted gross income, whichever is higher. People are exempt from the penalty if they have too little income or if the lowest-priced coverage available costs them more than 8.16 percent of their household income.

The I.R.S. had initially held off rejecting returns because the law was new, but then it delayed its plans to assess the effect of the executive order, said Nicole M. Elliott, a tax lawyer for Holland & Knight and a former I.R.S. official involved in putting into effect the Affordable Care Act.

“It is curious, given the executive order,” Ms. Elliott said. “It’s a little unclear where the agencies are going and how heavy-handed they will be in enforcing it.”

In evaluating its stance, the agency may have decided the requirement eases the burden on taxpayers by making it clear they need not worry if they have insurance or are exempt from the penalty, she said.

But the I.R.S. may still decide not to actively enforce the mandate, Ms. Elliott added. While the agency is taking steps to be sure it collects all the information necessary to levy the penalty, it could also take a very lenient view of how aggressively it goes after anyone who does not sign up. “It’s dangerous to read too much into this,” she said.

The White House declined to comment.

The I.R.S.’s decision to actively prepare to enforce the mandate only adds to the uncertainty about where the president stands about the future of the law. Just this month, he issued a second executive order aimed at allowing the sale of skimpier plans to both individuals and small businesses, the same day he announced he would abruptly stop funding subsidies for low-income individuals. He has abruptly switched positions on a new bipartisan proposal aimed at providing short-term stability to the insurance marketplaces under the law.

The proposed bill, drafted by Senators Lamar Alexander, Republican of Tennessee, and Patty Murray, Democrat of Washington, would restore the government subsidies called cost-sharing reductions for two years. While the draft legislation is unlikely to reduce insurance premium prices for 2018, it could serve to reassure jittery insurance companies that the law has a future beyond next year. On Friday, a group of health plans, hospitals and doctors, as well as the U.S. Chamber of Commerce, came out in support of the proposal.

The I.R.S. action does make it easier to see who should be buying coverage under the law, said Gary Claxton, an executive with the Kaiser Family Foundation. “This was the best way to enforce the mandate,” he said.

But much still depends on what happens next. As part of the second executive order he issued, Mr. Trump seemed to raise the possibility that the A.C.A. market could be further disrupted by the introduction of new plans that would not have to comply with the law. These plans, short-term policies sold to individuals and association plans sold to employers, would be much cheaper and offer far less coverage. If those plans were widely available, younger and healthier individuals and groups could buy them, causing turmoil on the exchanges and soaring prices for A.C.A. plans.

“That would be a bigger deal than this,” Mr. Claxton said.

Questions about ACA, private Medical Insurance and health insurance reimbursement? Physician Credentialing and Revalidation? or other changes in Medicare, Commercial Insurance, and Medicaid billing, credentialing and payments? Call the Firm Services at 512-243-6844