Lawmakers are so focused on ensuring people have access to health insurance that they’ve completely overlooked the root causes of medical care inflation.

Sean Williams (TMFUltraLong) Jul 8, 2017 at 6:49AM

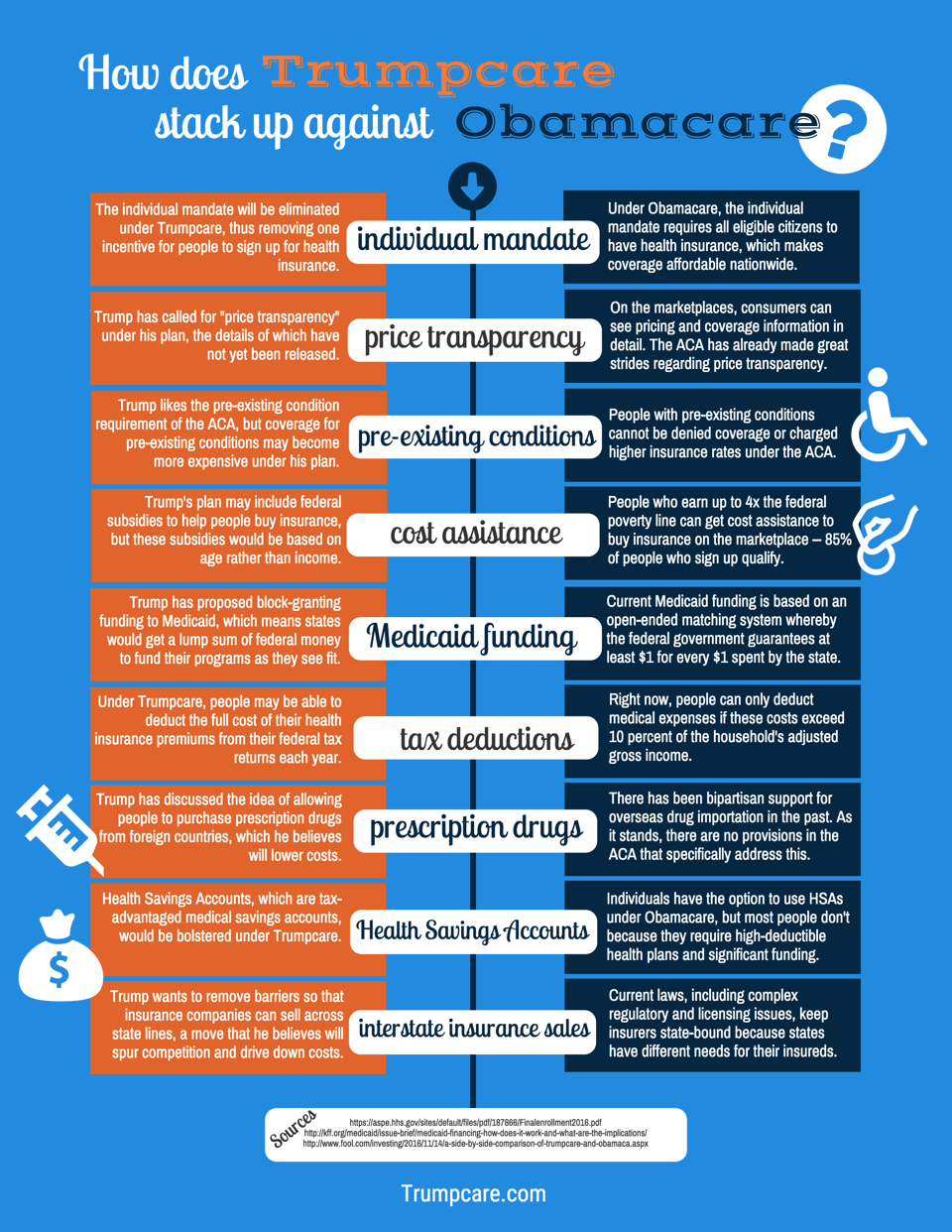

Who knew healthcare could be so complicated? Apparently not the president or Congress, as both are struggling to reach a consensus as to what to do with the future of healthcare in America.

Obamacare: Should it stay or should it go?

Obamacare, which is officially known as the Affordable Care Act (ACA) and was signed into law by Barack Obama in March 2010, has been controversial and mostly disliked since the start. However, it’s been successful in reducing the number of people without insurance. The expansion of Medicaid in 31 states, the provision of subsidies for low- and middle-income Americans, and insurance mandates that require member acceptance, regardless of pre-existing conditions, have been crucial in pushing the uninsured rate down to around 9% from 16%, according to data from the Centers for Disease Control and Prevention.

At the same time, Obamacare has had its shortcomings. The Shared Responsibility Payment (SRP), which is the penalty consumers pay for not purchasing health insurance, has been far too low relative to the cost of buying an annual health plan, thus fewer young, healthy people have enrolled than expected. The risk corridor, which was a fund designed to provide money to insurers with excessive losses that had set their premiums too low, also sputtered due to insufficient funding. With little in the way of financial protections for insurers, many big names have significantly reduced their ACA plan coverage in 2017 and beyond.

There are ways Obamacare can be fixed. These include adjusting the penalty on the SRP upward to more accurately reflect the cost of a health plan, and giving each state’s Office of the Insurance Commissioner more power to negotiate with insurers. Finally, Republicans can swallow their hubris and reinstitute the risk corridor. Fixing Obamacare isn’t out of the question, but it would force the GOP to break its promise of a repeal.

Is Trumpcare the answer to America’s healthcare woes?

Thus enters Trumpcare, which has actually taken on two forms already. First, we have the House Republican healthcare replacement plan known as the American Health Care Act (AHCA). A second version of the AHCA passed the House by a narrow margin in May and was sent along to the Senate.

More recently, the Senate introduced its own bill, the Better Care Reconciliation Act (BCRA), which proposes a number of changes to the healthcare landscape. Most notably, it would:

Include income-based subsidies, but reduce coverage to those earning up to 350% of the federal poverty level instead of 400%, as under Obamacare. Plus, older adults would be required to pay more under Trumpcare than under Obamacare.

Extend Medicaid expansion through 2020, but eventually eliminate it thereafter.

Extend cost-sharing reductions (CSR) through 2019, but end them thereafter. CSRs are the subsidies that help lower-income folks afford visits to the doctor by lowering copay, coinsurance, and deductible costs.

Allow for an essential health benefits waiver, with a twist. States can opt out of Obamacare’s mandate of 10 essential minimum health benefits per plan, but they won’t be able to repeal the community rating, which is the provision mandating that people of the same age and location are charged the same premium.

On one hand, Trumpcare may resolve a major issue with Obamacare. The additional freedoms in plan pricing for insurers should result in lower premiums over the next decade. These lower premiums are critical to attracting younger, healthier adults whose premium payments help offset the costs of treating sicker patients.

On the other hand, Trumpcare could be devastating to those on Medicaid or in need of CSRs, as well as the elderly. An estimated 22 million people are expected to lose coverage by 2026, according to the latest scoring by the Congressional Budget Office on the BCRA.

This mammoth issue won’t be fixed by Obamacare or Trumpcare

But regardless of whether or not Obamacare remains the law of the land, with modifications, or Republicans pass a new healthcare bill in Congress and anoint it as “Trumpcare,” neither plan is going to resolve the most pressing healthcare issue for Americans: the underlying cost of medical care.

Obamacare and Trumpcare both approach the same issue from different angles. Essentially, they aim to make health insurance more accessible to the average American. When Obamacare pulls the string, the middle class earning more than 400% of the federal poverty level finds it pricey to get insurance. Meanwhile, Trumpcare increases the costs of coverage for lower-income folks and the elderly.

What neither plan does is offer a solution to rising prescription drug inflation or the growing costs associated with medical procedures (e.g., surgeries). In other words, lawmakers are so focused on finding a way to ensure that everyone has access to health insurance that they’re completely overlooking the underlying cause of why health insurance costs are escalating in the first place.

We certainly don’t have to look far to find reasons why U.S. drugmakers are thriving. For starters, most drugs receive long periods of patent protection, keeping cheaper generic medicines on the sidelines. There’s also no universal health plan in the U.S., meaning Congress isn’t able to cap drug prices. Furthermore, a high standard of living in the U.S., as well as quicker access to new drugs, adds to drugmakers’ pricing power as well. Once new drugs are approved by the Food and Drug Administration, they can immediately find their way to pharmacy shelves. Finally, insurers rarely dispute list prices since they fear losing customers if they leave a popular drug off their approved formulary.

President Trump and a select few lawmakers on Capitol Hill have proposed tackling and lowering drug prices before, but none of these promises has gained any traction — nor are they likely to with tax reform still on the table in Washington.

Put plainly, until lawmakers deal with the underlying causes of prescription drug and procedural pricing inflation in the hospital and outpatient setting, their efforts to reform healthcare for the average American are likely to come up well short of their goal.

Questions about Medicare, Obamacare and reimbursement? Physician Credentialing and Revalidation ? or other changes in Medicare, Commercial Insurance, and Medicaid billing, credentialing and payments? Call the Firm Services at 512-243-6844